News

US infrastructure bill is one step closer after passing hurdle over weekend

The highly anticipated US Infrastructure Bill is one step closer to reality after it passed a key hurdle at the weekend

In what was a highly unusual event, the US Senate met over the weekend to discuss the bipartisan infrastructure bill.

The US Senate plans to pass the bipartisan infrastructure program in what will be a key part of President Biden’s policy agenda.

In a 67-27 vote, the final Senate consideration process is all that is left before the bill moves to the House.

Chuck Schumer says the final steps can be done the “easy way” or the “hard way”

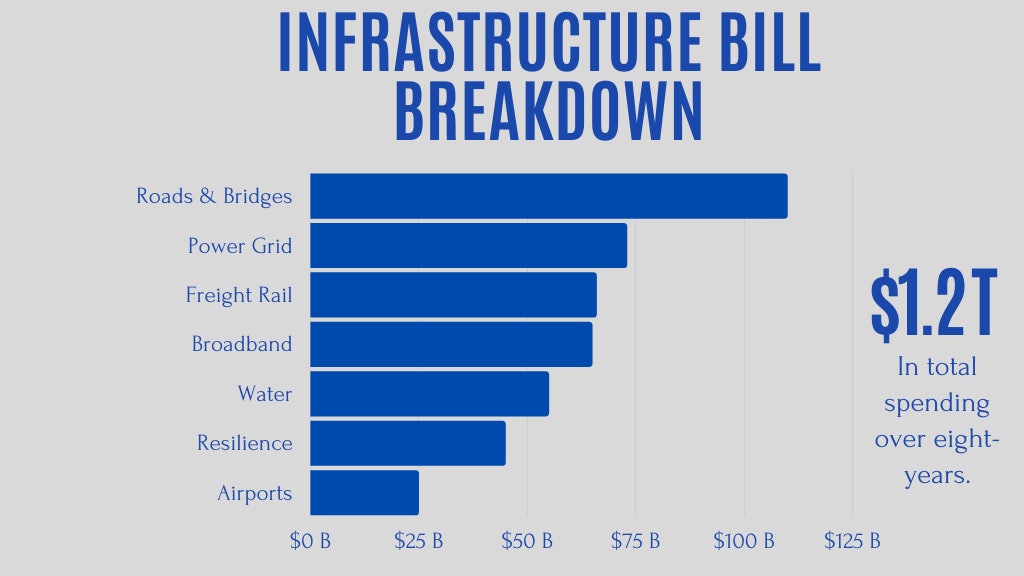

At its heart is a trillion-dollar program to help rebuild the backbone of the country; billions for public transit, passenger and rail freight, electric vehicle charging stations, ports and airports, water and wastewater pipes and facilities, environmental cleanup, the electric grids – and more.

As Biden has said: “This is a generational investment — a generational investment to modernize our infrastructure, creating millions of good-paying jobs — millions of good-paying jobs that position America to compete with the rest of the world in the 21st century.”

Bi-partisan support and cooperation

For the President, this bill means that Democrats and Republicans can work together; and that doing so shows that the country can come closer together.

The bill is so large that its benefits reach every state. The total cost in real dollars is bigger than what it took to build the US interstate highway system.

So Republicans supporting the deal will get political benefits too in their home states. And that is why enough Republicans are, for the first time, voting on major legislation initiated by Biden.

How will the infrastructure bill be funded?

But a funny thing happened on the way to the forum. A trillion dollars has to be paid for – at least in part. And so the other half of the bill outlines how the infrastructure builds will be funded.

There is unspent Covid-relief money from earlier rescue plans. Unspent unemployment insurance. The timing of a Medicare reimbursement rule. Revenues from spectrum auctions for 5G networks.

And $28 billion by strengthening tax enforcement of the cryptocurrency industry.

The world is on a steep learning curve on crypto, and crypto just got on the same treadmill with Washington.

Washington shorts on crypto

The proposed legislation would expand reporting of broker revenues from crypto

transactions and would also subject elements of the crypto blockchain to greater exposure on capital gains.

At the heart of the debate is how broadly to apply new tax rules to crypto brokers. And it’s not a partisan issue.

There are Republicans and Democrats who want more discipline on the industry, and anti-regulation Republicans and pro-privacy Democrats who want no change from the status quo.

And some Democrats believe crypto coin creation is a massively energy intensive process – so there is a global warming tinge to the controversy. Who knew?

This will be resolved in the Senate – but not for long

Anything in the Senate bill has to get through the House.

And the head of the Securities and Exchange Commission said recently that the agency wants to take a good hard look at the rules that should apply to crypto.

But back to the main game: Biden’s agenda for the country is much bigger than just infrastructure, and being prepared for immediate work in the Senate is a $3.5 trillion bill addressing education, health care, climate change and other Democratic priorities.

Republicans will not back this broader legislation

Republicans have refused to advance bills on voting rights, police reform, gun control and other issues at the heart of racial justice and social equity.

Taken as a whole, the Biden program is the most ambitious legislative agenda for the country since Franklin Roosevelt’s New Deal, and Lyndon Johnson’s Great Society. And it will take near-unanimity among Democrats to pass it.

Biden knows that the passage of all these bills – not just the spending programs but the racial justice issues too – is crucial not just for the county, but for his presidency. And for Democrats in Congress too.

-

News3 days ago

News3 days agoSix nations pledge security for Strait of Hormuz

-

News3 days ago

Energy markets face turmoil from Iranian attacks

-

News3 days ago

Apple to earn over $1B in AI app fees

-

Tech3 days ago

Uber to invest $1.25 billion in Rivian robotaxis

-

Tech4 days ago

Australian scientists create world’s first quantum battery

-

Tech9 hours ago

Meta to cut 20% workforce for AI focus

-

News2 days ago

Oil prices surge on Middle East supply disruptions

-

News4 days ago

Germany and France warn against Iran war escalation