Money

Tax tips to boost your tax returns!

For Business, the best way to reduce your tax in Australia this year, is to take a closer look at the federal budget. Ticker’s money expert Dr Steven Enticott takes a look.

Treasurer Josh Frydenberg announced the government would be extending temporary full expensing and temporary loss carry-back (to the year 2019) for an additional year until 30 June 2023.

Further, Mr Frydenberg said the government will deliver more than $16 billion in tax cuts to small and medium businesses by 2023-24 with around $1.5 billion flowing in 2019 20.

This, he said, includes reducing the tax rate for small and medium companies, from 30 per cent in 2014 15 to 25 per cent from 1 July 2021.

Prepay your expenses where you can and don’t be too hasty getting out your invoices prior to June 30 even more so if it’s been a great income year. Its also a great time to purchase a business asset of any value to really boost your returns (or lower your tax bills!).

Stocktakes can be counted on Cost price, Replacement Price or even Actual values which is one of our greatest tax planning tools for those that carry stock. Get counting!

For Employees make sure you have paid for all your work-related expenses prior to June 30. Try to bring costs forward when you’ve had a great income year to smooth the tax pains.

Don’t forget – Sunglasses, Hats and Sunscreen for taxpayers that work in any outdoor occupation (including driving) they are tax deductible – Keep the receipts!

Claim Everything

This one each year is a bit tongue in cheek, though correctly claiming expenses is our expertise. Your job is to think of absolutely anything that has a connection with your incomes and let us measure the appropriateness of claim.

For Investors with repairs and maintenance on investment properties?Consider bringing forward so you can enjoy your tax deduction in the current financial year amongst other costs!

Pre-paying interest Say,on a loan of $300,000 it may cost $12,000 but it could get you up to $6000 back as a tax refund this year. Requires a negotiation with your lender!!

Made a capital gain during the past year, for example, the sale or part sale of a business (including investments the business has made), shares or a property.

If the answer is a ‘yes’ then you should be thinking about your options for managing the CGT liability.

Start by looking for capital losses (not hard at the moment) to offset the CGT liability (or losses carried forward from prior years) and consider selling out losses before June 30 to offset gains – call to discuss.

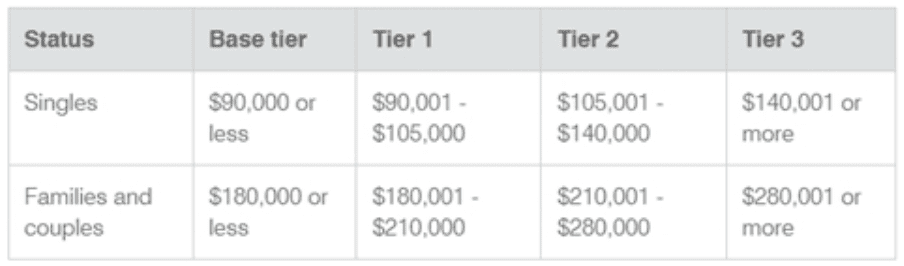

Medicare levy surcharge & Private Health Insurance Rebate thresholds

For the rates of Medicare levy surcharge that applies or the amount of rebate you are entitled to see the rebate and surcharge levels applicable are:

• Single parents and couples (including de facto couples) are subject to family tiers.

• For families with children, the thresholds are increased by $1,500 for each child after the first.

Superannuation

Whilst there are no major changes for 2021 tax year the scheduled ones are going ahead.

• The Superannuation Guarantee rate is increasing to 10%, effective 1 July 2021

• From July 1st 2021 the concessional cap into super rises to $27,500 which includes super SG and salary sacrifices. Don’t forget personal super contributions can also be claimed as a deduction under the same limit.

• For under 67’s they may be able to also contribute $300,000* Non-Concessional all at once.

• For over 67’s they will need to pass the work test and be restricted to $100,000. Forget about it over 75 sadly.

• The limits rise to $110,000 annually and $330,000 for 3 years (below 67’s) from 1 July 2021

Superannuation has become so complex

We recommend that you never contribute until you’ve cleared it with your advisors first.

Super contributions to be claimed in this tax year they need to be paid WELL before June 30 (i.e., by mid-June – Do it Now!) and yes in many cases you should contribute to super for example;

An average earner saves around 20% of tax on their contribution so even if they put the money into the safe cash option of the fund, they have already had one great investment year!

However, if you are bit on the younger side burdened with a lot of bad debt then speak to us about doing the numbers on super contributions before you do.

Make larger super contributions

if you haven’t used all of your concessional cap in an earlier year. If you make or receive concessional contributions (CCs) of less than the annual concessional contributions cap of $25,000 pa, you may be able to accrue these unused amounts for use in subsequent financial years.

Unused cap amounts can be carried forward for up to five years before they expire.

2018/19 was the first financial year you could accrue unused cap amounts. To be eligible to make catch-up CCs, your total super balance at the prior 30 June must be below $500,000.

Superannuation Co-contributions for super is something you should still DO. Up to a 50% matching rate on up to $1,000 of after-tax contributions, so a maximum amount $500 FREE from the ATO into your super!! Income thresholds must be below $54,837

Superannuation Pensions remember, you need to have made your annual drawdowns by June 30 and the good news for 2020 and 2021 the minimum amount to drawdown has been halved. Maximum drawdown limits are unchanged.

Superannuation Spouse Contribution of $3000

The amount of the offset is 18 per cent of the spouse contribution you make (max. offset of $540) reducing your own tax. Spouse income must be under $37,000 to get the full offset, then it gradually reduces to zero at $40,000.

Again, there are always other conditions so check with CIA first or your Superfund to avoid disappointment.

You can watch Ticker Money weekly with Steve Enticott and Mike Loder on Ticker News.