Money

Do declining household deposits point to recession?

The Australian economy is facing a potential full-blown recession as indicated by the decline in household deposits held by Australian banks, which raises concerns about the financial stability of households. However, there is optimism for a potential recovery in late 2024 or 2025.

The recent interest rate hikes and soaring inflation rates have instilled caution in consumers, causing them to adopt a more frugal approach to their spending habits.

This has resulted in a noticeable deceleration in household spending and a decrease in deposits. This is having a direct impact on businesses, with those seeking assistance from administrators and insolvency firms, rising by an alarming 50% in the past three months alone.

These developments pose significant concerns for the Reserve Bank of Australia (RBA) as they grapple with the intricate task of addressing these challenges. It is imperative that they carefully assess the repercussions of these circumstances on the overall stability of the Australian economy.

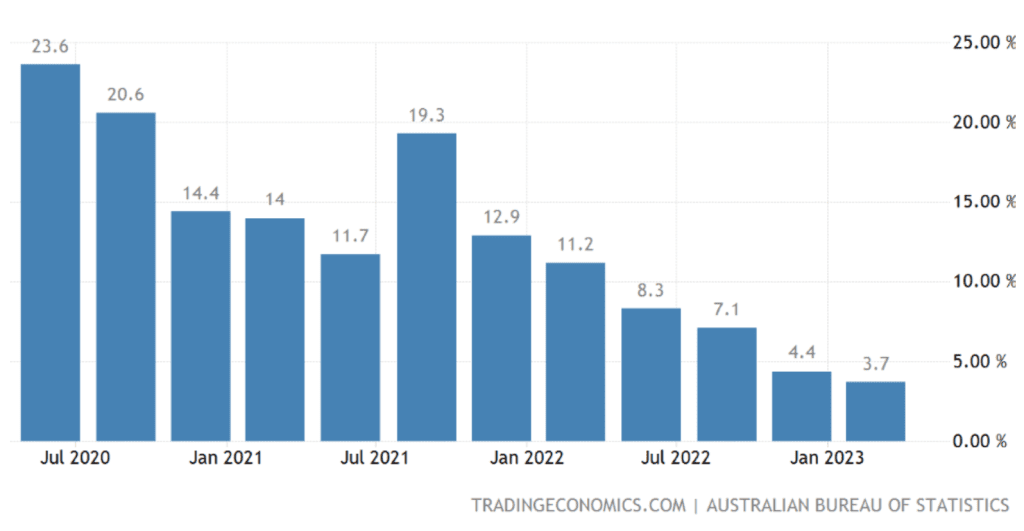

According to the Australian Prudential Regulation Authority (APRA), household deposits across the banking system experienced a significant decline of $7.76 billion in June, representing a drop of 0.56%. This decline marks the sixth consecutive quarterly decrease in the household savings ratio (calculated by dividing household savings by household disposable income), reaching its lowest level in nearly 15 years.

Households now have a savings ratio of less than 3.7%, which is significantly lower than the usual running average of 5%.

To better understand the significance of this decrease, it is important to note that in December 2021, the housing savings ratio stood at a significant 13.5%.

This was primarily due to the substantial savings accumulated by households during the pandemic lockdowns.

The diminishing value of household deposits is a clear indication that more households are feeling the financial strain caused by the monetary policies implemented by the RBA.

As household spending continues to outpace income growth, Australian households are increasingly forced to dip into their savings, as evidenced by the significant increase of 11.5% in interest paid on mortgages during the last quarter.

The decline in the household savings ratio and the necessity to tap into savings to cover expenses highlights the challenges faced by many households in the current economic climate.

This raises concerns about the sustainability of household finances and the potential impact on overall economic stability.

It is essential for the RBA to consider the delayed effects of interest rate hikes on mortgage holders and adopt appropriate measures to alleviate the financial burden on households and businesses.

Consumer sentiment remains negative, which can be attributed to the risks posed to personal finances.

Retail spending has experienced a decline for three consecutive quarters, indicating the cautious approach adopted by consumers.

While Australia lags slightly behind the United States in the global inflation picture, similar dynamics are observed, with sticky services inflation and a robust labour market.

However, Australia’s unique factors, such as minimum wage increases, rent, and utilities frameworks, present additional challenges to the economy.

Even if inflation is brought within the 2-3% target range, prices will remain higher than they were 12 months ago and can be expected to continue rising. This trend is expected to have an ongoing impact on the savings ratio.

-

Shows1 day ago

Shows1 day agoDave Fraser discusses 25 years of supply chain evolution

-

News1 day ago

Europe faces wildfires, heatwaves, droughts, and hail

-

Shows20 hours ago

Channel 10 considers outsourcing news amid industry cuts

-

Shows3 days ago

Hover Energy’s innovation in renewable energy integration

-

News1 day ago

Ukraine names new military commander amid protests

-

Leaders3 days ago

Reforming Australia’s payments infrastructure for fintech innovation

-

News3 days ago

Burnham becomes PM, promises to rewire Britain

-

News4 days ago

Two U.S. troops killed in Iran missile attack